The Modern Carbon Economy: Fragmented Markets, Digital MRV Expansion, and the Growing Crisis of Trust in Carbon Accounting

OHK analyzes today’s carbon ecosystem, decoding fragmentation, technology adoption, and why credibility concerns now dominate global climate markets.

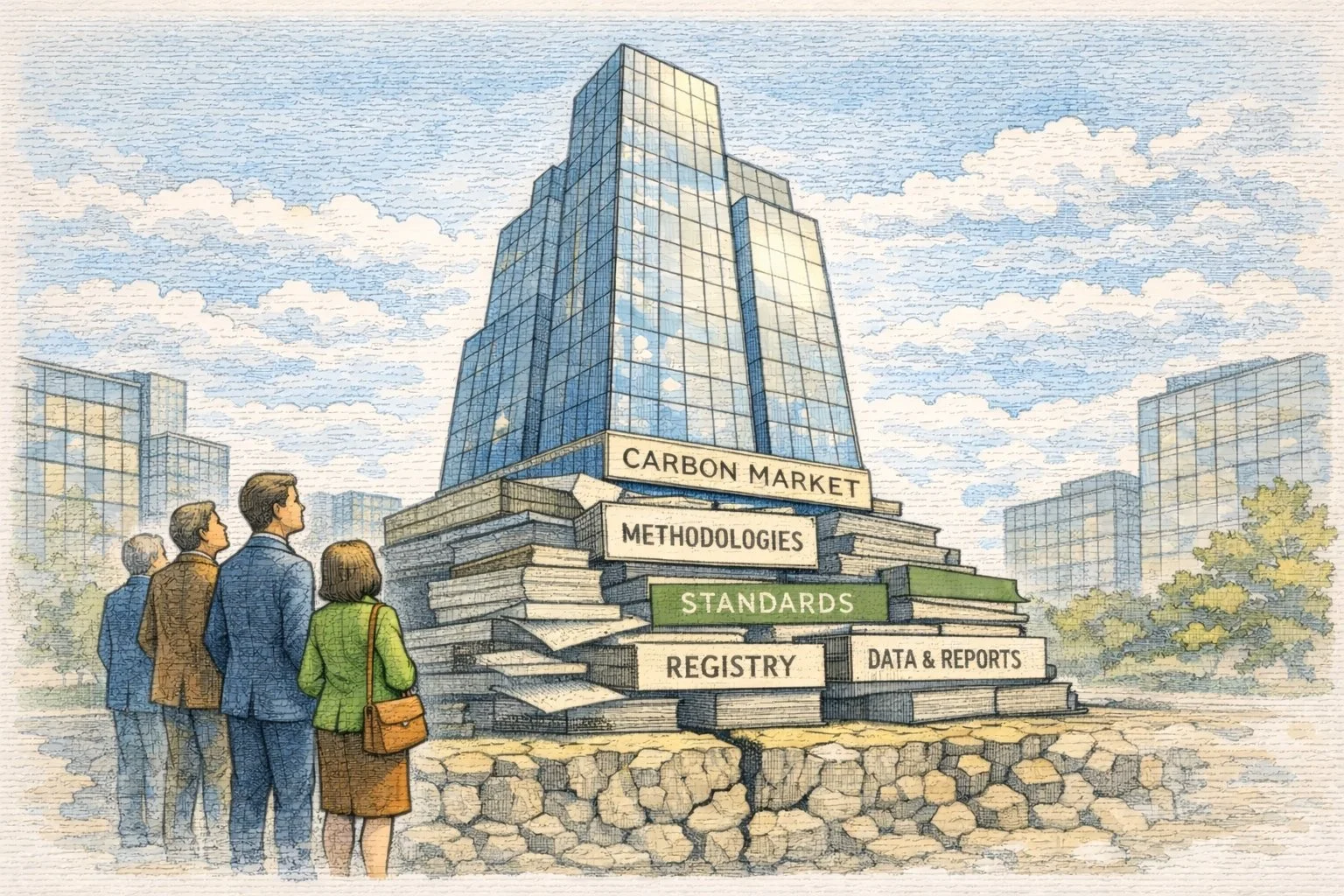

This illustration shows a gleaming carbon market rising skyward but its foundations are built on stacked paper systems of methodologies, standards, registries, and reports, quietly revealing how today’s climate finance architecture rests on fragile documentation rather than real-time, verifiable infrastructure.

This article, Part II, represents the second installment in a four-part series on carbon markets, climate accounting, and the digital systems supporting decarbonization efforts. Following the exploration of how incentive-driven design shaped early carbon markets, this piece assesses the current landscape of compliance regimes, voluntary credits, corporate net-zero commitments, and rapidly expanding digital MRV tools. The next article investigates the structural limitations of most carbon software platforms, before the series culminates in OHK’s integrated approach to carbon infrastructure development. Refer to Part I here and Part III here.

In essence, this is a key part of OHK’s structural trilogy on carbon:

• Part I — Carbon Markets: Incentive architecture and economic distortion

• Part II — Carbon Accounting: Measurement systems, technology scaling distortions, digital MRV, and modeled emissions

• Part III — Carbon Infrastructure: Software architecture built around processes rather than systems, institutional governance design, and programmable integrity

Reading Time: 45 min.

All illustrations are copyrighted and may not be used, reproduced, or distributed without prior written permission.

Summary: Part II analyzes the current carbon landscape, highlighting the fragmentation of standards, proliferation of registries, and accelerating digitization of measurement and reporting processes. It explores how technologies such as satellite monitoring, automated MRV, and AI-driven estimation have improved speed and scale while failing to resolve fundamental challenges around data quality, verification, auditability, and institutional coherence. The article also examines the growing crisis of trust in carbon credits, rising regulatory scrutiny, and increasing buyer skepticism, showing how technological progress has outpaced the governance structures required for credible markets.

As carbon markets digitize and scale, fragmented standards, AI-driven monitoring tools, and proliferating registries promise unprecedented speed and visibility. Yet beneath the dashboards and satellite feeds, structural gaps persist. Credits move faster than verification frameworks evolve, and interoperability lags behind innovation. On one side, data multiplies and transactions accelerate; on the other, confidence strains under inconsistent methodologies and uneven quality controls. The bridge labeled “trust” begins to crack not from lack of technology, but from the absence of coherent system architecture capable of aligning speed, scale, and integrity in a unified carbon economy.

The New Carbon Marketplace: Compliance, Voluntary Credits, and the Struggle for Credibility

As carbon markets moved beyond Kyoto-era treaty mechanisms, they did not disappear but instead diversified, decentralized, and expanded into a far more complex ecosystem driven by regulatory compliance systems, corporate climate commitments, and voluntary offset markets operating in parallel. The why shifted from intergovernmental burden sharing toward embedding carbon into domestic policy instruments and corporate decarbonization strategies. The how evolved into cap-and-trade systems, internal carbon pricing, and large-scale offset purchasing to meet climate pledges. The where spread across Europe, North America, Asia, and emerging economies, while voluntary project development concentrated heavily in the Global South. The when accelerated sharply after the Paris Agreement, as governments tightened emissions targets and corporations announced net-zero commitments at unprecedented scale.

Within compliance markets, regulators placed hard caps on total emissions and distributed or auctioned allowances that firms could trade, embedding carbon pricing directly into national economic frameworks. This worked by creating predictable price signals, incentivizing reductions where cheapest, and integrating climate policy into mainstream economic planning. What did not work was the persistence of political constraints, uneven ambition across jurisdictions, and limited geographic coverage, leaving large portions of global emissions outside regulated systems and driving continued reliance on offsets to bridge the gap between policy ambition and economic feasibility.

Alongside regulated markets, voluntary carbon markets expanded rapidly as corporations sought flexible pathways to meet climate commitments, offset residual emissions, and demonstrate environmental leadership. Companies purchased credits tied to renewable energy, forest conservation, reforestation, soil carbon, and emerging removal technologies, channeling billions of dollars into climate projects outside formal regulatory systems. This worked by mobilizing private capital at unprecedented speed and responding to corporate climate pressure faster than policy cycles allowed. What failed was consistent quality control, as integrity varied widely across standards, methodologies, and project types, creating a fragmented landscape where environmental outcomes became difficult to compare, verify, or trust.

A clear illustration of this modern fragmentation is how today’s carbon economy operates simultaneously across large compliance systems such as the EU Emissions Trading System, which now covers roughly 40 percent of the European Union’s total emissions and has driven covered-sector emissions down by about 50 percent since 2005, alongside rapidly expanding voluntary markets that corporations use to meet net-zero pledges outside regulatory caps, where annual credit purchases surged above $1 billion globally before declining amid integrity concerns in 2023, showing both scale and stress at once. This dual structure worked by embedding carbon pricing into public policy while mobilizing private capital far beyond government programs, but it failed by creating parallel markets with different quality thresholds, fragmented governance, and inconsistent verification logic, leaving buyers, regulators, and the public navigating a landscape where some credits are backed by strict regulatory enforcement while others depend on voluntary standards and varying assumptions, ultimately amplifying trust challenges even as market volume and technological sophistication increased.

Proliferation of Standards and Registries: How Fragmentation Replaced Coherent Market Architecture

This illustration portrays a fragmented carbon marketplace unfolding across parallel standards and registries, each operating under its own methodologies, verification rules, and governance logic—accelerating innovation and market growth while quietly eroding comparability, interoperability, and systemic trust. What appears as diversification from above reveals structural fragmentation beneath, where credits cannot be easily reconciled, assumptions vary across rulebooks, and the absence of shared infrastructure turns climate finance into a patchwork of silos rather than a coherent global architecture.

After the decline of centralized Kyoto mechanisms, carbon markets did not converge around a single successor system, but instead fractured into dozens of standards, registries, certification bodies, and verification frameworks, each offering its own methodologies, governance rules, and quality thresholds. The why was speed and innovation, as private actors filled regulatory gaps left by slow multilateral reform. The how involved creating independent rulebooks for project approval, credit issuance, monitoring, and verification. The where spanned global markets, with different standards dominating different regions and sectors. The when accelerated rapidly after 2015, as voluntary markets expanded to meet corporate demand.

This fragmentation worked by enabling experimentation, faster approvals, and tailored methodologies for new sectors such as nature-based solutions and carbon removal. However, it failed by replacing systemic coherence with governance silos, where credits issued under different standards could not be easily compared, stress-tested, or integrated into a shared integrity framework, creating opportunities for arbitrage, confusion, and uneven quality across markets.

Interoperability remained largely absent. There was no shared data backbone, no unified verification logic, and no cross-market analytics layer capable of evaluating credit performance across standards. What worked was market flexibility and innovation speed. What failed was system-level transparency and trust, as fragmentation weakened the ability to assess environmental outcomes consistently at scale.

A concrete measure of this fragmentation is visible in how today’s voluntary carbon market operates across more than a dozen major standards and registries, including Verra’s Verified Carbon Standard, Gold Standard, American Carbon Registry, Climate Action Reserve, and several regional systems, which together have issued over 2 billion carbon credits cumulatively, yet under widely different methodological rules and verification thresholds, meaning that two forest conservation projects in neighboring countries can generate credits using entirely different baseline assumptions, permanence buffers, and leakage accounting models. This worked by allowing rapid growth and sector experimentation, particularly in nature-based solutions that now account for over 40 percent of voluntary market credit issuance by volume, but it failed by creating non-comparable environmental assets traded under the same “carbon credit” label, where buyers struggle to distinguish high-integrity projects from inflated or low-impact ones, leading major corporations and investors in recent years to publicly suspend or scale back offset purchases amid quality concerns, illustrating how the absence of a unified market architecture enabled volume expansion while systematically undermining trust and coherence across the carbon economy.

The Digital MRV Boom: When Climate Measurement Finally Went High-Tech

Digital tools transformed how carbon is measured, replacing sporadic site audits with real-time satellite data, automated sensors, and continuous reporting systems that dramatically expanded scale and visibility across global carbon markets, even as these high-tech layers were built atop legacy methodologies and fragmented governance structures that technology alone could not fix.

Following years of credibility crises, carbon markets entered a period of rapid technological adoption, particularly in measurement, reporting, and verification. The why was cost reduction, scalability, and demand for faster verification cycles. The how involved satellite monitoring, remote sensing, AI-based emissions estimation, and automated reporting platforms. The where expanded globally, especially in land-use projects and nature-based solutions. The when accelerated after 2018, as digital tools matured and investor pressure for transparency intensified.

Satellite imagery enabled continuous monitoring of forest cover, land-use change, and ecosystem conditions, while AI models translated remote data into estimated emissions outcomes. Automated dashboards replaced many manual reporting workflows, dramatically reducing transaction costs and increasing measurement frequency. This worked by expanding coverage, lowering barriers to entry, and enabling near-real-time project tracking compared to the episodic audits of the Kyoto era.

What did not work was the assumption that faster data automatically produced higher integrity. Many digital systems simply automated flawed methodologies, embedding the same baseline assumptions, counterfactual modeling, and verification weaknesses into software pipelines, effectively scaling distortions at digital speed rather than correcting them.

The scale of the digital MRV expansion is visible in the rapid adoption of satellite-based monitoring platforms, AI-driven emissions estimation tools, and automated climate data pipelines, with Earth observation providers now capturing daily high-resolution imagery of over 90 percent of the planet’s land surface, enabling near-real-time tracking of deforestation, land-use change, methane plumes, and industrial activity that previously relied on annual site audits. For example, methane monitoring satellites launched in the past five years have identified tens of thousands of previously unreported emission events globally, while remote sensing platforms supporting forest carbon projects now process petabytes of environmental data annually to estimate biomass change and carbon flux across millions of hectares. This worked by dramatically lowering monitoring costs, increasing measurement frequency from years to days or weeks, and expanding coverage to remote regions previously inaccessible to auditors, but it failed by digitizing estimation rather than transforming verification, as most AI models still rely on assumptions, proxy indicators, and probabilistic inference layered on top of baseline methodologies rather than direct emissions measurement, meaning that while data volume and speed exploded, the underlying integrity challenges of modeled reality versus actual climate impact largely remained intact.

The illustration depicts a scattered tower of drones, sensors, dashboards, and cloud systems rising from the ground like a technological monument to progress, capturing how carbon markets have rapidly adopted digital tools to monitor emissions, automate reporting, and expand project scale across the globe. Yet the jumble of disconnected devices reveals a deeper truth: while measurement has gone high-tech, the underlying governance and integrity architecture remains fragmented and improvised. Each tool optimizes speed and efficiency in isolation, but together they form no coherent system of trust, illustrating how today’s carbon technology stack accelerates existing methodologies without resolving the structural weaknesses of baselines, additionality, and verification that continue to undermine market credibility.

The Emerging Carbon Technology Stack: Tools Without System Architecture

As carbon markets expanded beyond early treaty mechanisms and corporate climate commitments accelerated after 2015, a rapidly growing ecosystem of digital tools emerged to modernize how emissions were measured, reported, verified, and traded, giving rise to what is now commonly referred to as the carbon technology stack. The why was operational necessity, as spreadsheet-based reporting and consultant-driven audits could no longer support the scale, speed, and geographic complexity of modern climate markets. The how involved venture-backed software platforms, satellite data providers, AI-driven emissions models, digital registries, and automated reporting systems designed to streamline data flows and reduce transaction friction. The where spanned global markets, with strong concentration in North America and Europe alongside data collection focused heavily in the Global South. The when accelerated sharply between 2019 and 2024, during which more than $8–10 billion in venture capital flowed into climate and carbon software companies, reflecting the rapid financialization of climate data infrastructure.

At the measurement layer, hundreds of digital MRV platforms now ingest corporate activity data, energy consumption records, supply chain information, satellite imagery, and sensor feeds to estimate emissions across facilities and projects. Corporate carbon accounting software alone has grown into a multi-billion-dollar market, with over 1,000 active platforms globally offering automated Scope 1, 2, and 3 calculations, emissions forecasting, and compliance reporting aligned with frameworks such as the GHG Protocol and emerging regulatory disclosure regimes. At the project level, remote sensing providers deploy constellations of satellites capable of monitoring deforestation, land-use change, methane plumes, and industrial activity at near-real-time frequency, generating petabytes of environmental data annually used to estimate carbon fluxes across millions of hectares of land and thousands of industrial sites.

Above raw data collection, artificial intelligence and statistical modeling tools increasingly translate observational data into emissions estimates, baselines, leakage models, permanence risk scores, and credit issuance projections. Machine learning systems now simulate forest growth rates, soil carbon sequestration, avoided deforestation scenarios, and industrial emissions trajectories across decades, often processing millions of data points per project to generate carbon credit volumes at scale. These tools dramatically reduce the cost and time required to generate project documentation, enabling credit issuance cycles that once took years to be completed in months or even weeks, fundamentally reshaping the speed of market participation.

Parallel to MRV digitization, registry and trading infrastructure has also modernized. Dozens of digital registries now issue, track, transfer, and retire carbon credits across voluntary and compliance markets, often supported by blockchain-based ledgers, API integrations, and automated settlement systems designed to prevent double counting and improve transaction efficiency. Global carbon trading volumes now reach billions of credits annually, with digital platforms enabling near-instant ownership transfers that mirror modern financial clearing systems rather than legacy environmental reporting processes.

Taken together, the modern carbon technology stack now spans four primary functional layers:

digital MRV and data ingestion systems, AI-driven modeling and emissions estimation engines, registry and transaction infrastructure, and corporate carbon management platforms integrating compliance, procurement, and disclosure. In operational terms, carbon markets today are vastly more digitized than their Kyoto-era predecessors, processing orders of magnitude more data at dramatically lower marginal cost.

Yet despite this technological sophistication, the stack evolved as a collection of productivity tools rather than as a coherent integrity system. Each layer largely optimizes for workflow efficiency, cost reduction, and market scalability within its own functional silo. Measurement platforms estimate emissions but rarely connect directly to registry issuance logic. Registries track ownership but do not validate scientific plausibility. AI models generate projections without embedded governance oversight or systemic cross-project benchmarking. Corporate accounting tools report footprints without independent verification architecture beyond periodic audits.

Digitization improved throughput — not trust.

The result is a carbon infrastructure that resembles a rapidly assembled fintech ecosystem without a central banking system: highly efficient at moving data and assets, yet lacking unified verification logic, systemic risk controls, or real-time integrity assurance across the full lifecycle of emissions measurement and credit issuance. While billions of dollars now flow through technologically advanced climate platforms, the underlying governance model remains structurally similar to early carbon markets — reliant on modeled assumptions, fragmented oversight, and episodic verification rather than continuous, programmable integrity.

In essence, modern carbon markets did not fail to digitize. They digitized almost everything — except the system of trust itself. Tools scaled faster than governance architecture, software optimized speed before integrity, and platforms automated workflows without embedding systemic verification. The emerging carbon technology stack successfully solved operational friction, but left the foundational political economy problem of climate data credibility largely untouched, setting the stage for today’s widening trust crisis despite unprecedented technological advancement.

Where Technology Helps: Speed, Scale, and Visibility

From left to right, the illustration traces the modern digital journey of carbon measurement and market visibility. On the left, a field technician kneels in agricultural soil, inserting a carbon sensor while satellite imagery and rising data charts hover overhead, symbolizing the shift from periodic site audits to continuous, technology-enabled measurement of emissions and sequestration. In the center, the planet is wrapped in glowing data networks layered over cities, forests, and infrastructure, representing the explosion of digital MRV systems that aggregate satellite feeds, sensor data, and project reports into real-time climate intelligence platforms. On the right, an analyst monitors carbon market dashboards filled with live emissions metrics, project performance indicators, and trading data, showing how raw environmental measurements now flow directly into digital accounting systems and market decision-making. Together, the sequence illustrates how technology has dramatically accelerated speed, expanded geographic scale, and increased visibility across carbon markets—transforming climate data from slow, paper-based reporting into continuous global digital infrastructure.

Modern digital infrastructure has materially transformed the operational mechanics of carbon markets, particularly in measurement frequency, geographic reach, transaction efficiency, and marginal cost reduction. Unlike the Kyoto-era system, where monitoring often occurred once every one to three years through site visits and consultant-authored reports, contemporary digital MRV platforms can ingest data continuously from smart meters, industrial control systems, IoT sensors, and satellite feeds. In energy and industrial sectors, emissions data can now be processed monthly, weekly, or even daily, reducing reporting latency by more than 70 percent compared to traditional audit cycles.

Cost reductions have been equally significant. Across renewable energy, landfill methane, and industrial efficiency projects, digital measurement and reporting systems have reduced monitoring and verification costs by an estimated 50–80 percent, particularly where automation replaces travel-intensive site audits and manual spreadsheet modeling. What once required teams of consultants assembling documentation over three to six months can now be processed algorithmically within days or weeks. Cloud-based reporting environments allow thousands of projects simultaneously to upload structured datasets through standardized templates rather than bespoke PDF reports, dramatically lowering transaction friction and accelerating credit issuance timelines.

Geographic scale has expanded even more dramatically. Satellite-enabled forest monitoring platforms now track millions of hectares in near real time, replacing small field sample plots with wall-to-wall coverage across entire jurisdictions. Optical and radar satellite systems can detect deforestation events within 5–10 days, while methane-detection satellites are capable of identifying industrial leaks at concentrations as low as 25 kilograms per hour, a level of visibility that was technically impossible under periodic on-site inspections. Instead of discovering land-use change years later during verification reviews, platforms can now generate automated alerts triggered by pixel-level vegetation change algorithms.

Transaction infrastructure has similarly modernized. Digital registries process credit issuance and transfers within hours rather than weeks, while API integrations allow corporate carbon accounting software to synchronize procurement, retirement, and disclosure data automatically. Large multinational companies now manage tens of thousands of suppliers through centralized emissions dashboards, integrating Scope 1, 2, and 3 reporting into enterprise systems rather than maintaining disconnected spreadsheets. Disclosure cycles aligned with regulatory frameworks can be populated directly from internal ERP systems, reducing compliance preparation time by 30–60 percent in many reporting organizations.

Transparency potential has also increased. Public dashboards now allow stakeholders to view project locations, methodologies, and issuance records in real time. Open-access satellite imagery provides visual confirmation of forest cover, land-use change, and fire events. Digital registries reduce double counting within a platform by creating immutable transaction logs. Compared to the opaque, document-heavy systems of the early 2000s, today’s ecosystem offers orders of magnitude more observable data.

Collectively, these advances have allowed carbon markets to scale operationally at unprecedented speed. Project pipelines can expand more rapidly. Capital can move more efficiently. Monitoring coverage is broader and more frequent. Administrative barriers are lower. Digital systems have undeniably transformed carbon markets from paper-based administrative programs into data-intensive financial ecosystems capable of handling billions of dollars annually. However, it is critical to understand what these systems were primarily optimized to do: increase speed, reduce cost, and expand throughput.

Most digital MRV platforms automate existing methodologies rather than redesign them. Automated engines apply approved baseline formulas faster, but they do not independently test whether those baselines are economically realistic. Satellite monitoring increases visibility of forest cover change, but it does not automatically resolve additionality, leakage, or permanence risk. Registries prevent double counting within a database, but they do not create cross-standard comparability across fragmented markets.

In effect, technology strengthened operational efficiency and surface transparency, while leaving deeper governance architecture largely intact. It made markets faster. It made them cheaper. It made them more visible. What it did not automatically make them was structurally trustworthy.

Technology optimized performance metrics. It did not automatically optimize system integrity.

Where It Fails: When Software Digitizes Weak Market Design

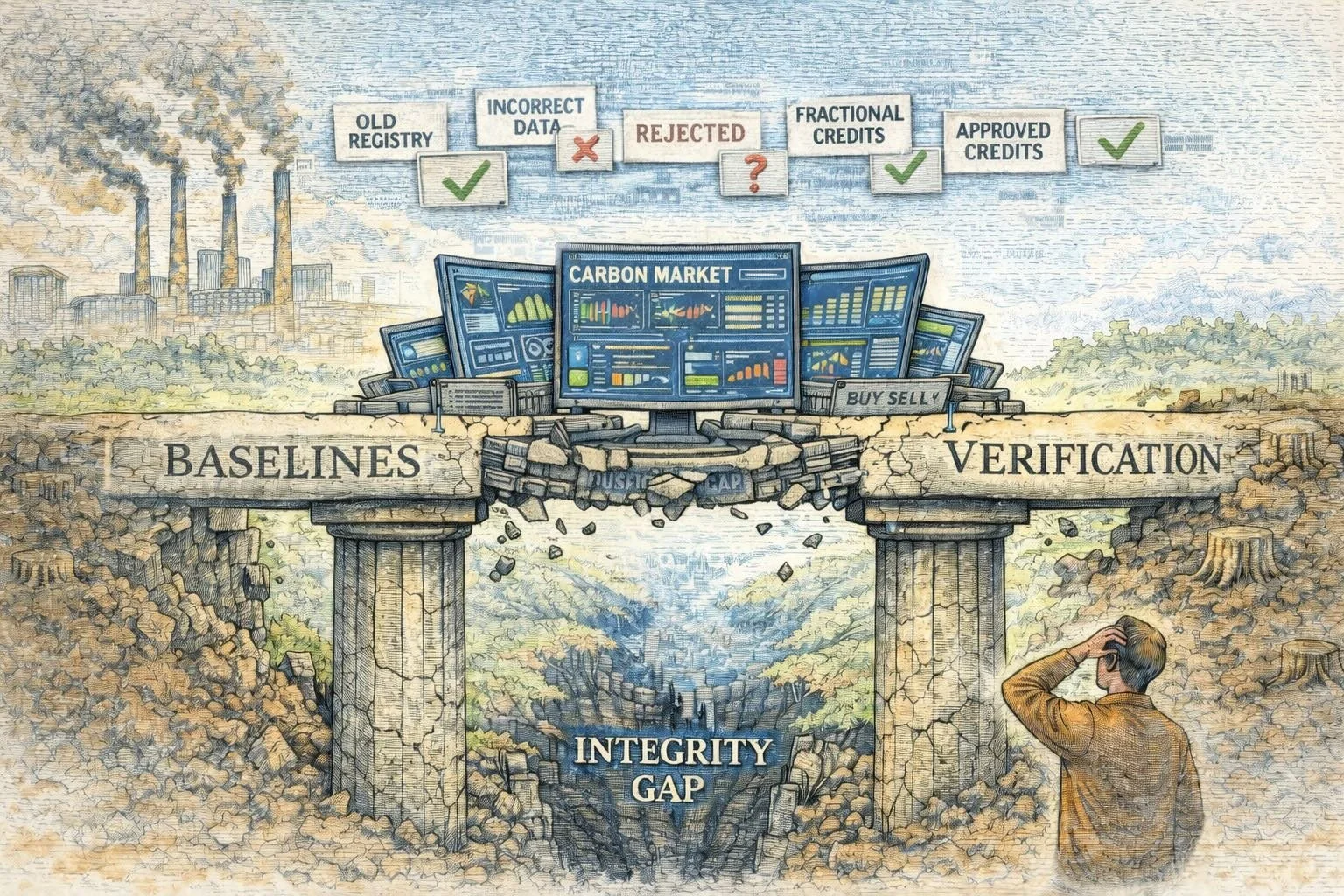

The illustration depicts a crumbling stone bridge labeled Baselines and Verification straining under the weight of glowing dashboards and automated carbon data systems, while smokestacks rise on one side and a scarred, deforested landscape stretches across the other, illustrating how digital platforms have accelerated measurement and trading without repairing the fragile foundations of market design—where flawed assumptions, rejected methodologies, and opaque approvals collapse faster when software amplifies them, leaving observers to confront the widening gap between technological speed and environmental credibility.

Despite dramatic gains in automation, most digital carbon platforms have focused on digitizing existing workflows rather than rebuilding the underlying integrity architecture of carbon markets. Baseline formulas that were once applied manually in spreadsheets are now executed instantly by software engines. Additionality assessments that previously relied on consultant-written narratives are now embedded into standardized digital questionnaires. Model-based emissions estimates that were once reviewed episodically are now generated continuously by algorithms. The problem is not speed. The problem is that the same weak assumptions were simply encoded into faster systems.

In practice, this meant that flawed methodologies scaled more efficiently. If a baseline projection overstated emissions by 20–50 percent, automation did not correct it — it multiplied it across thousands of projects. If an additionality test relied on subjective financial scenarios, digital tools merely standardized the narrative rather than verifying economic reality. Where early markets issued millions of questionable credits slowly, modern platforms can now issue tens or hundreds of millions annually using the same structural logic, accelerating volume without strengthening environmental certainty.

This produced a textbook garbage-in, garbage-out dynamic, where higher data velocity amplified distortions rather than resolving them. Faster MRV did not inherently improve accuracy — it improved throughput. Continuous satellite monitoring could confirm land cover change, but not whether a forest was truly under threat in the absence of carbon finance. Automated energy models could calculate avoided emissions, but not whether those reductions were economically inevitable anyway. Speed substituted for scrutiny.

Artificial intelligence tools have further deepened this challenge. Many AI-driven estimation platforms now generate emissions baselines, forest biomass calculations, and leakage projections using proprietary machine-learning models trained on historical datasets. While these systems increase scale and reduce human labor, they often introduce model opacity, where underlying assumptions are no longer visible even to auditors. Instead of transparent spreadsheets that could be manually inspected, stakeholders now confront black-box predictions with confidence intervals but limited interpretability. In some platforms, more than 70–90 percent of emissions estimates are now algorithmically generated rather than directly measured.

What worked was operational efficiency, global scalability, and cost compression. What failed was auditability, economic realism, and system-level integrity. Digital tools became extremely good at executing rules; they were never designed to question whether the rules themselves produced credible climate outcomes.

Weak methodologies, once digitized, did not disappear—they industrialized.

Weak rules × fast software = accelerated distortion.

Instead of fixing the structural flaws of carbon accounting, much of today’s climate tech stack has unintentionally transformed them into high-throughput automated systems—proving that technology can dramatically increase market volume without increasing environmental truth.

The Trust Crisis: Markets Scaling Into Credibility Limits

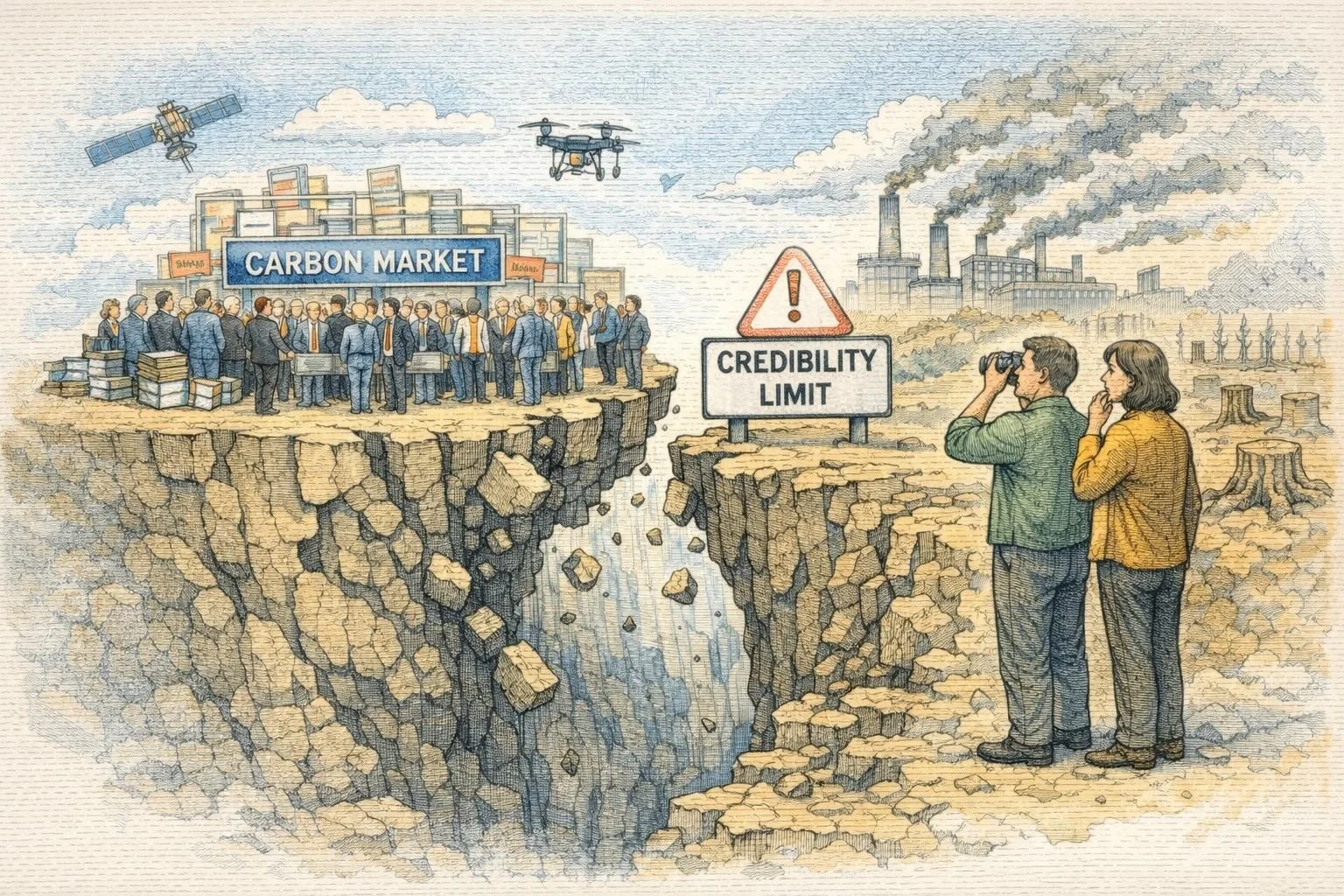

The illustration depicts a crowded carbon marketplace racing toward the edge of a crumbling cliff, where booming transactions and expanding participation continue uninterrupted, even as the ground beneath them fractures and falls away. Across the widening gap, a warning sign marks the approaching limits of credibility, watched by observers who can already see the environmental damage accumulating in the distance. Satellites and drones hover overhead, symbolizing modern monitoring tools that expand visibility but cannot repair structural weakness. The scene captures how carbon markets have scaled rapidly in volume and sophistication while trust, integrity, and governance struggle to keep pace—revealing a system growing faster than its foundations can support.

As digital tools accelerated issuance and project pipelines multiplied, credit volumes began expanding faster than confidence in their environmental reality, pushing integrity concerns from technical circles into mainstream climate and financial debate. Academic meta-analyses, investigative journalism, and regulatory reviews increasingly showed that a substantial share of offsets delivered little or no additional climate benefit, particularly across large renewable projects, industrial baselines, and many nature-based solutions. Studies examining voluntary forest credits found that in some major programs over 70–90 percent of issued credits likely did not represent real emissions reductions, while reviews of earlier offset mechanisms had already demonstrated systemic over-crediting across entire sectors. What had once been framed as isolated quality issues was now recognized as a structural market problem.

Nature-based offsets became a central flashpoint. Satellite evidence revealed that many forest conservation projects credited for “avoided deforestation” were located in areas with historically low deforestation risk, meaning forests were unlikely to be cut down regardless of carbon finance. Permanence risks emerged as wildfires, illegal logging, and land-use pressures reversed credited carbon storage within years of issuance. Some large conservation portfolios lost 10–30 percent of credited forest carbon stocks in single fire seasons, directly challenging the assumption that offsets represented long-term climate mitigation. At the same time, baseline inflation continued across both technological and land-use projects, as modeling choices systematically overstated counterfactual emissions trajectories, inflating credit volumes while masking weak real-world impact.

Corporate buyers responded quickly. Major multinationals paused or scaled back offset purchases, internal climate teams raised reputational risk concerns, and procurement standards tightened dramatically. Surveys of corporate sustainability leaders between 2022 and 2024 showed that more than half reduced or delayed offset use due to integrity uncertainty, while demand shifted sharply toward higher-cost removal credits perceived as more durable. At the regulatory level, governments introduced stricter eligibility rules, enhanced disclosure requirements, and tighter claims guidance around net-zero marketing. Voluntary market oversight bodies launched sweeping reforms, including new quality principles, standardized integrity benchmarks, and credit-rating systems intended to separate high-quality projects from inflated ones.

What worked was a long-overdue surge in scrutiny, transparency, and reform momentum. What failed was the underlying market architecture, which had allowed volume, speed, and automation to scale decades ahead of systemic governance, economic verification, and digital integrity infrastructure.

The crisis did not emerge because technology moved too fast; it emerged because markets scaled before trust systems were built. Baseline-driven valuation, subjective additionality, fragmented standards, and workflow-focused software had created a high-throughput credit engine with limited capacity to ensure real climate outcomes. By the time integrity alarms became impossible to ignore, hundreds of millions of credits were already circulating through global markets, embedding risk into corporate climate strategies and public policy frameworks alike.

Scale without integrity produced liquidity.

Liquidity without credibility produced collapse.

The modern carbon economy thus reached a structural ceiling: it could grow in volume, but not in trust — revealing that without foundational systems of verification, governance, and programmable integrity, even the most technologically advanced climate markets will eventually run into their credibility limits.

Synthesis: Tools Scaled Markets Faster Than They Built Trust

Across today’s carbon ecosystem, a clear structural pattern has emerged. Technology dramatically improved speed, scale, visibility, and transaction efficiency, but it was layered on top of market designs built around hypothetical baselines, subjective additionality, fragmented standards, and document-based governance. Digital MRV, satellite monitoring, AI estimation tools, and automated registries did exactly what they were engineered to do: accelerate issuance, lower costs, and expand project pipelines globally. What they were never designed to do was question whether the underlying economic and methodological assumptions produced real, durable climate impact.

As a result, old integrity weaknesses did not disappear in the digital era — they scaled. Baseline inflation became faster. Questionable additionality became standardized. Fragmented standards multiplied more efficiently. Model-based assumptions became harder to audit once embedded inside black-box algorithms. The carbon technology stack optimized throughput, not truth. Markets grew in volume precisely because friction was removed, yet credibility eroded because governance capacity did not evolve at the same pace.

The modern trust crisis did not arise from bad actors alone. It emerged from structural misalignment between financial scale and integrity infrastructure. Markets were designed to move capital quickly. Software was designed to automate existing rules. But neither was built to continuously verify economic realism, permanence, systemic risk, or climate outcomes at scale. Speed became the performance metric. Volume became the success signal. Integrity remained largely procedural.

Digitization without architectural reform produced efficiency — not trust.

Automation without systemic verification produced scale — not credibility.

In essence, Part I showed how incentives and institutional design embedded distortion into early carbon markets. Part II reveals how modern technology amplified those same structural flaws rather than correcting them. The carbon economy did not fail because tools were insufficient. It strained because markets scaled before systems of trust were built.

Weak market design → digitized at scale → accelerated credibility breakdown.

Digitization → Faster scaling → Integrity strain → Trust crisis

Bridge to Part III: If Part I revealed how incentive design embedded structural distortion, and Part II showed how modern technology scaled those distortions into a credibility crisis, Part III confronts the core problem directly: why today’s carbon software ecosystem focuses on digitizing workflows instead of building systems of trust. The next section explores the infrastructure gap at the heart of carbon markets, examining what real integrity architecture requires and why most climate tech platforms are not designed to deliver it.

At OHK, we view the modern carbon economy not as a failure of technology, but as a lesson in what happens when markets digitize faster than integrity architecture evolves. The credibility crisis facing today’s carbon markets is not the result of insufficient tools, data, or automation. It is the structural outcome of scaling workflows, issuance, and measurement speed on top of fragmented standards, assumption-driven methodologies, and governance systems never designed for real-time verification at global scale. By understanding how digital MRV, AI estimation, and automated registries amplified existing weaknesses rather than correcting them, OHK approaches climate infrastructure as a systems challenge, where trust must be engineered into market design itself, and where integrity architecture must grow alongside efficiency, transparency, and scale rather than lag behind them.

At OHK, our work on carbon markets, climate accounting, and digital climate infrastructure is grounded in building real-world systems of integrity, not standalone software tools. We support governments, development institutions, and private-sector leaders in designing credible carbon accounting frameworks, full-stack digital MRV platforms, registry infrastructure, and governance mechanisms that enable transparent, scalable decarbonization. By combining institutional reform expertise with advanced data systems and software architecture, we help organizations move beyond fragmented reporting toward trusted climate infrastructure. If your organization is developing carbon accounting systems, engaging in carbon markets, or building digital climate platforms, contact us to explore how OHK can support the design and implementation of resilient, policy-ready carbon infrastructure.